Rise and shine everyone.

We had quite the eventful day yesterday with the Fed chanign up their changing up their statement, followed by earnings from Microsoft, Meta and Tesla. We cover that in a bit.

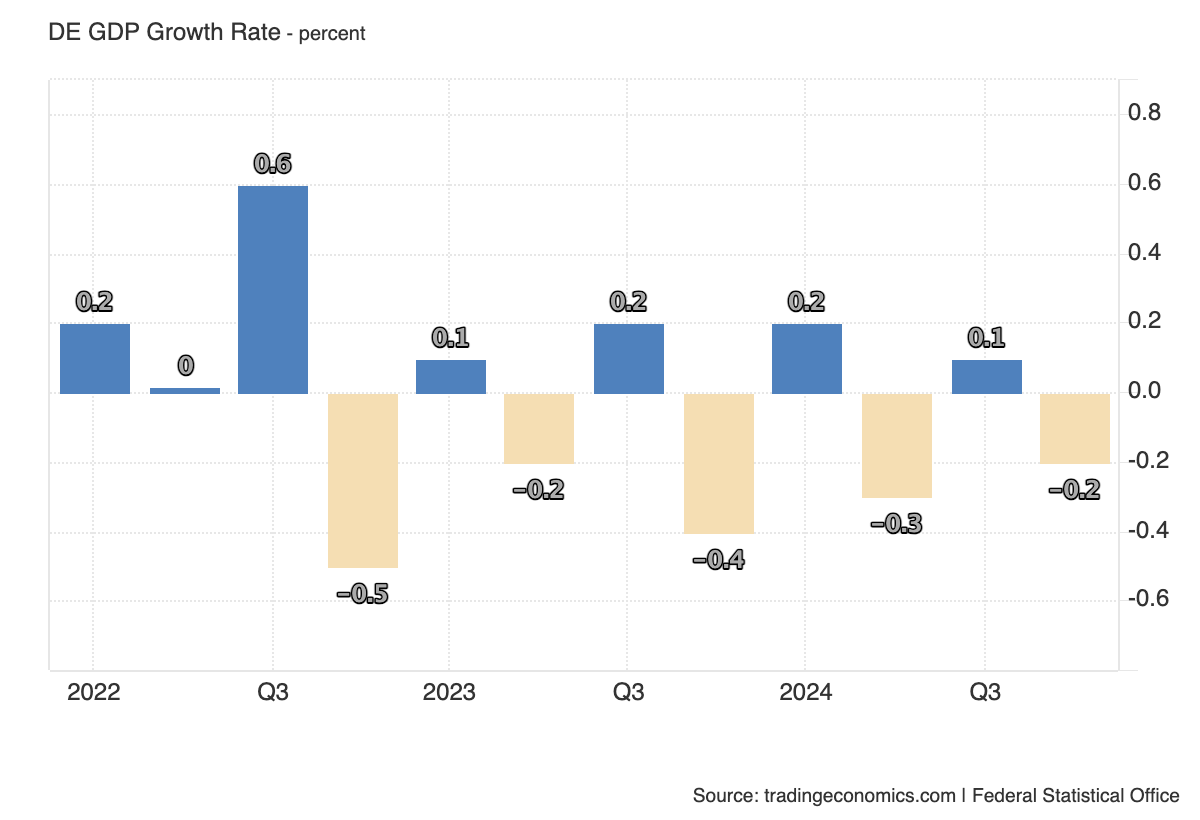

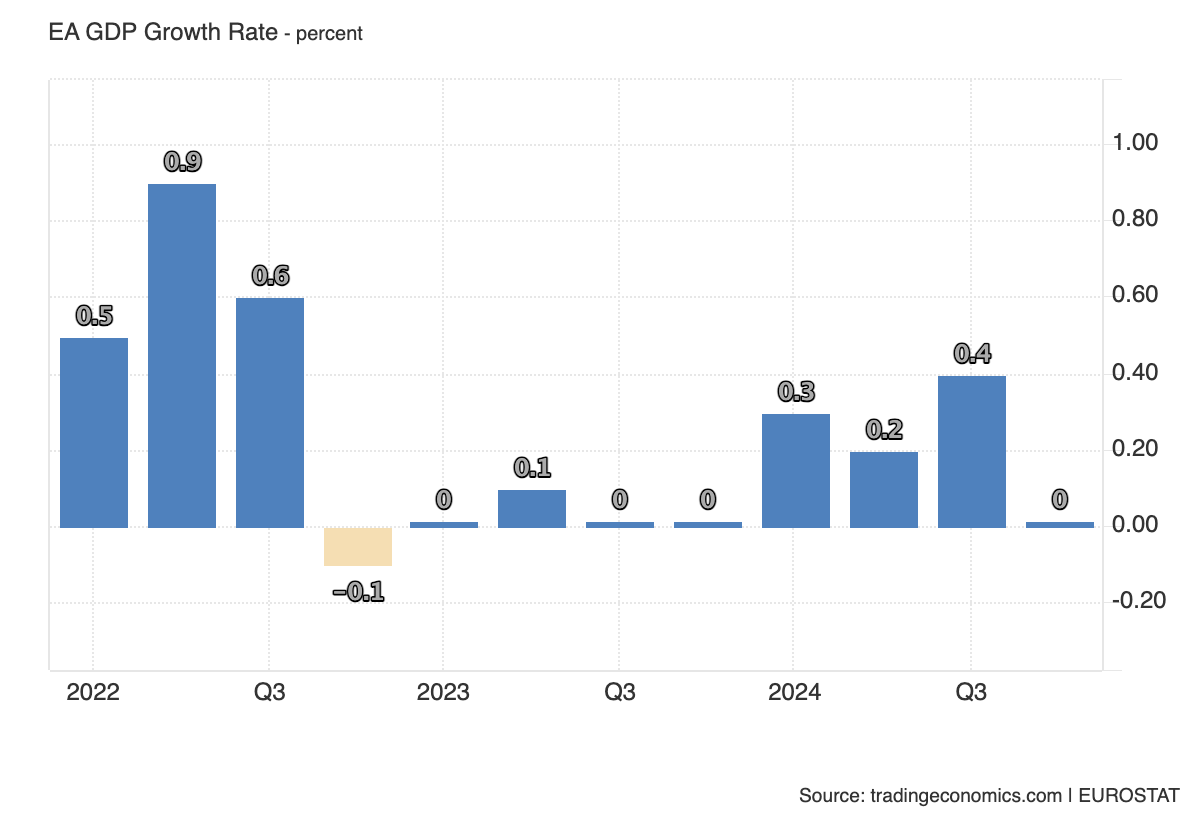

Coming up today, we have the ECB’s rate decision. Last week brought us some optimistic data from the EA in terms of improving PMIs, particularly in manufacturing. But GDP growth numbers came in today - Eurozone, Germany and France all showed a contraction.

Given this, we expect the ECB will deliver a 25-bps cut today, and possibly three more cuts this year to bring the rate closer to neutral, i.e., 2-2.25%.

However, should this trend of improving PMIs continue, we think there may be a discussion to slowdown rate cuts. The ECB has discussed an abundance of caution and the negative effects that US Foreign Policy could have resulting in trade wars and higher inflation, which could certainly add to the decision to slowdown.

Chair Powell

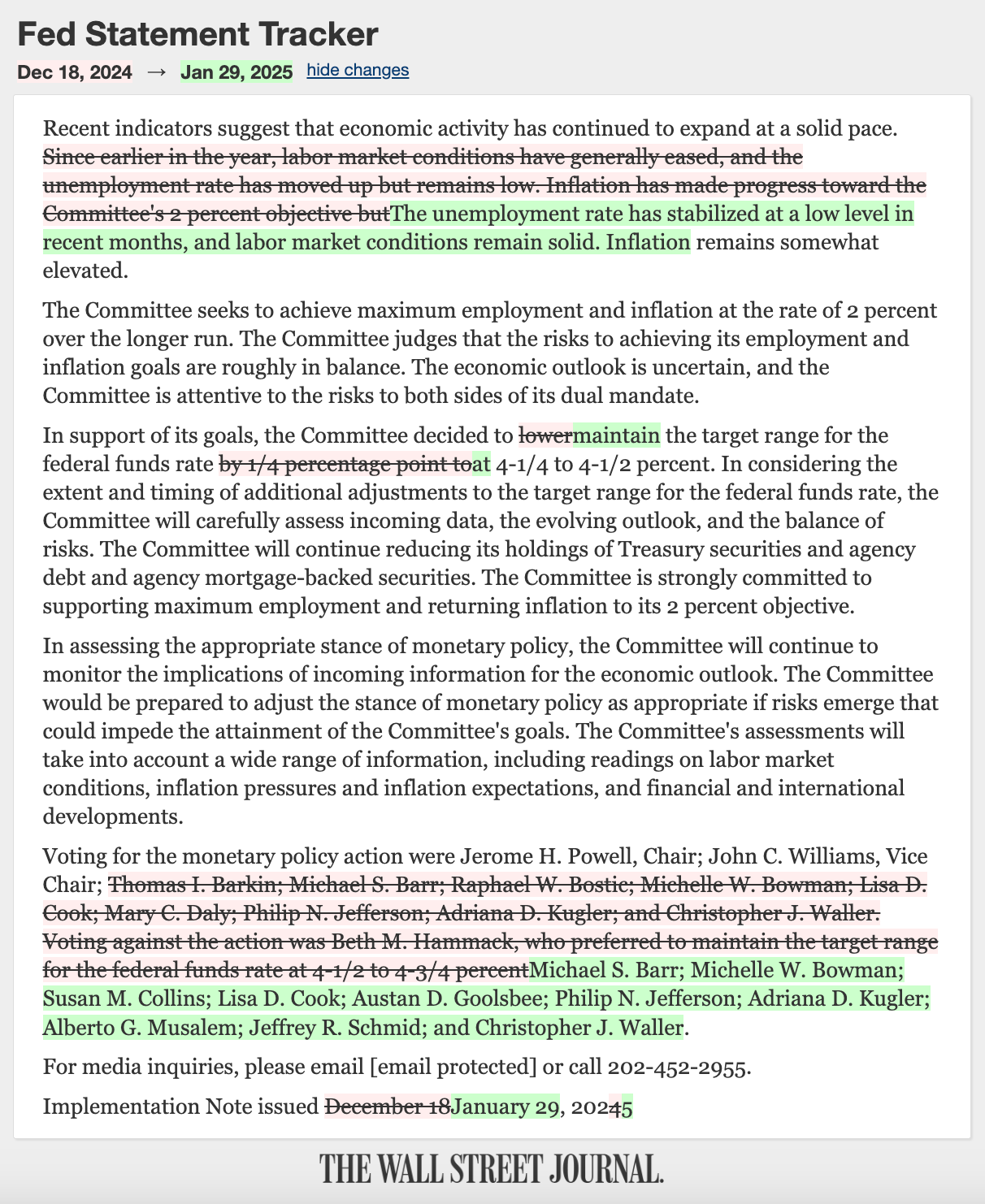

The change to the Fed’s statement was glaring. There is now a clear focus on inflation and it shows that the Fed may even be a little worried. While Chair Powell wrote off the changes as a “language clean up”, we think that there is a definite message that the Fed is sending. And that is: We’re not getting rate cuts any time soon. The next cut will likely come in the summer - June or July, if these conditions persist.

While Chair Powell tried to avoid any political discussion and maintained a neutral stance, there was a hint of worry about tariffs. He remained neutral but also mentioned that rates were restrictive enough, giving us the idea that a hike is quite likely not coming. There were some discussions of a hike in the markets.

But, all in all, they’ve confirmed that they are “in no hurry” to cut rates, and while they don’t inflation to decelerate to 2%, they do want to see a sustainable path lower.

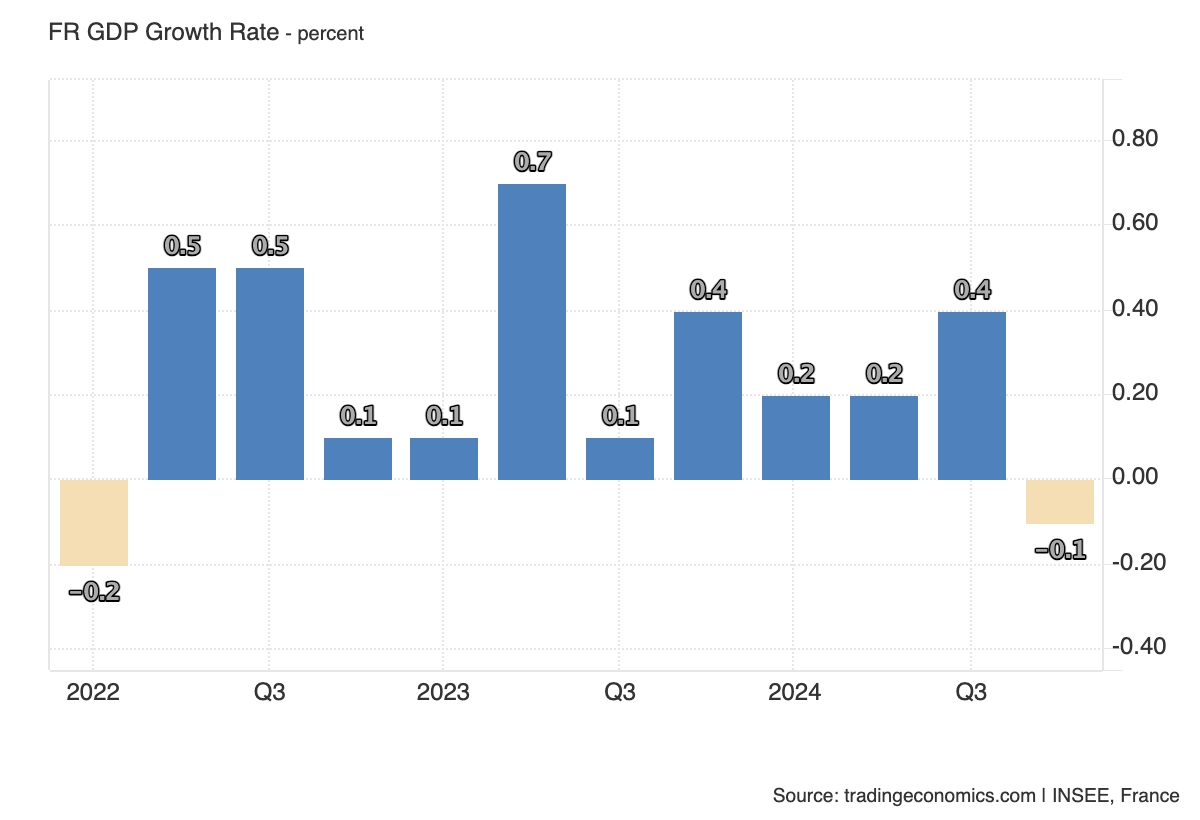

GDP - Eurozone, Germany, and France contracted

The German economy contracted by 0.2% in Q4 2024, worse than expected, as weak exports outweighed gains in consumption, marking a full-year decline of 0.2%. Structural issues, high energy costs, and weak investment continue to weigh on growth, prompting the government to cut its 2025 forecast to 0.3% from 1.1%.

The Eurozone economy stalled in Q4, missing forecasts, with contractions in Germany (-0.2%) and France (-0.1%), stagnation in Italy, and a sharp 1.3% drop in Ireland, while Spain (0.8%) and Portugal (1.5%) posted solid growth. Year-on-year, the Eurozone grew 0.9% in Q4, with full-year expansion at 0.7%, improving from 0.4% in 2023.

Meanwhile, France’s economy shrank 0.1% in Q4, its first contraction since early 2022, as weak investment, slowing consumption, and negative trade balance offset earlier growth. Full-year GDP rose 1.1%, in line with 2023. With upcoming elections in Germany and economic headwinds persisting, business leaders are expected to push for lower energy costs and tax relief.

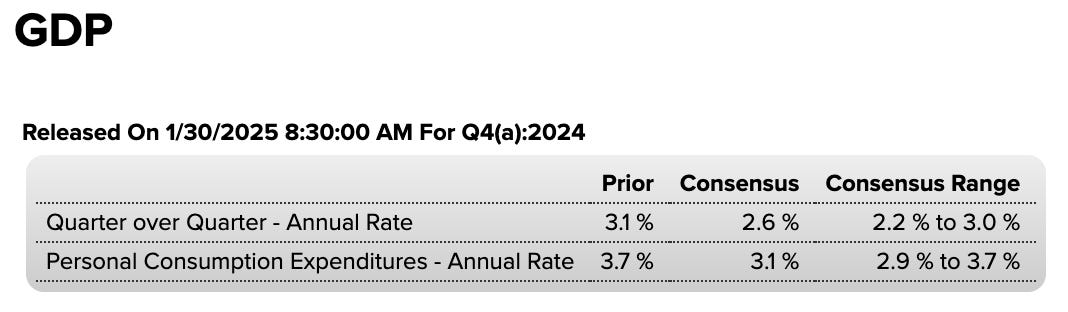

GDP - US forecasted to contract

We get US Real GDP growth advance estimates later today at 8:30 am ET. The consensus is for a QoQ growth of 2.6%, below the 3.1% achieved in the previous quarter. Atlanta GDP now has the estimate at 2.3%, while Goldman Sach predicts 1.8%.

Growth will likely be supported by strong consumer spending, a rebound in residential investment, and slower import growth, while export moderation, weaker business investment, and a -0.8pp drag from inventory accumulation due to hurricanes and strikes will weigh on the overall figure. GDP growth is anticipated to increase in Q1, 2025, driven by resilient consumption, robust fixed investment, and front-loaded imports ahead of potential tariff increases, with severe weather effects largely offsetting.

Earnings - Microsoft, Tesla and Meta

Microsoft is still trading lower in the pre-market, as the numbers for Azure came in at the lower end of their guidance. Microsoft announced that DeepSeek’s R1 artificial intelligence model is now available on its Azure AI Foundry platform and GitHub. This integration allows businesses to seamlessly incorporate advanced AI capabilities into their operations. There wasn’t much discussed about DeepSeek being an actual competitor but rather these models becoming commoditized.

For Tesla, Elon Musk announced plans to launch a paid robotaxi service in June, despite declining earnings and vehicle deliveries. While Q4 results missed estimates, Tesla shares rose on Musk’s bullish outlook, including advancements in AI, autonomy, and humanoid robots. The company provided little detail on its long-promised affordable models but remains optimistic about future growth. Musk largely avoided politics during the earnings call, though Tesla CFO warned of potential risks from tariffs. Analysts see Musk’s political influence as a regulatory advantage, particularly for Tesla’s self-driving ambitions.

Investors seemed to like what Meta had to say. Meta CEO Mark Zuckerberg expressed confidence in the company’s AI strategy, predicting Meta AI will be the industry’s leading assistant in 2025, reaching over a billion users. Despite a lower-than-expected Q1 revenue forecast, Meta’s Q4 sales beat expectations at $48.4 billion, driven by strong ad revenue. The company plans to invest heavily in AI, aiming to cut costs and enhance engineering automation. Meta is also adjusting its policies under the Trump administration, rolling back diversity efforts and fact-checking, while strengthening ties with conservative figures. Shares rose after Zuckerberg’s remarks, despite concerns over high AI spending and competition from China’s DeepSeek.

Chart of the Day - Fed Statement Tracker

What We’re Watching Today

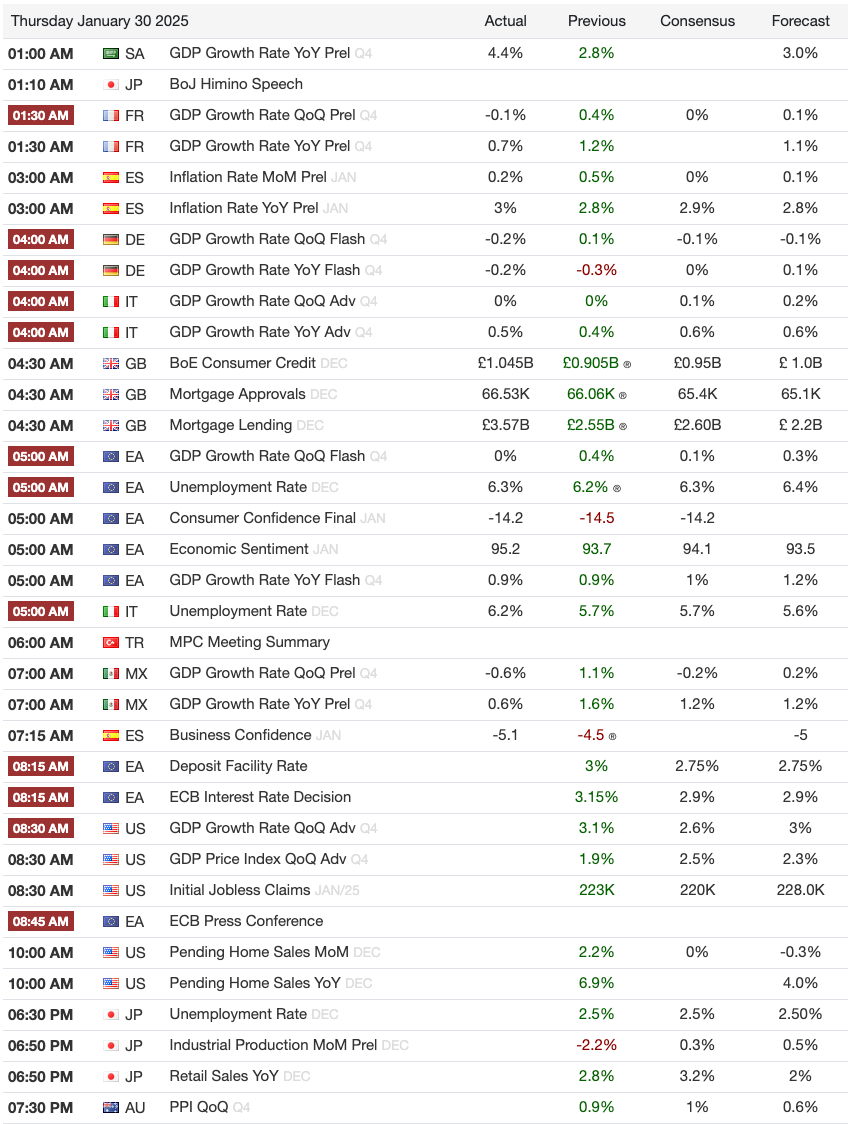

ECB Rate Decision at 8:15 am ET

US GDP Numbers at 8:30 am ET

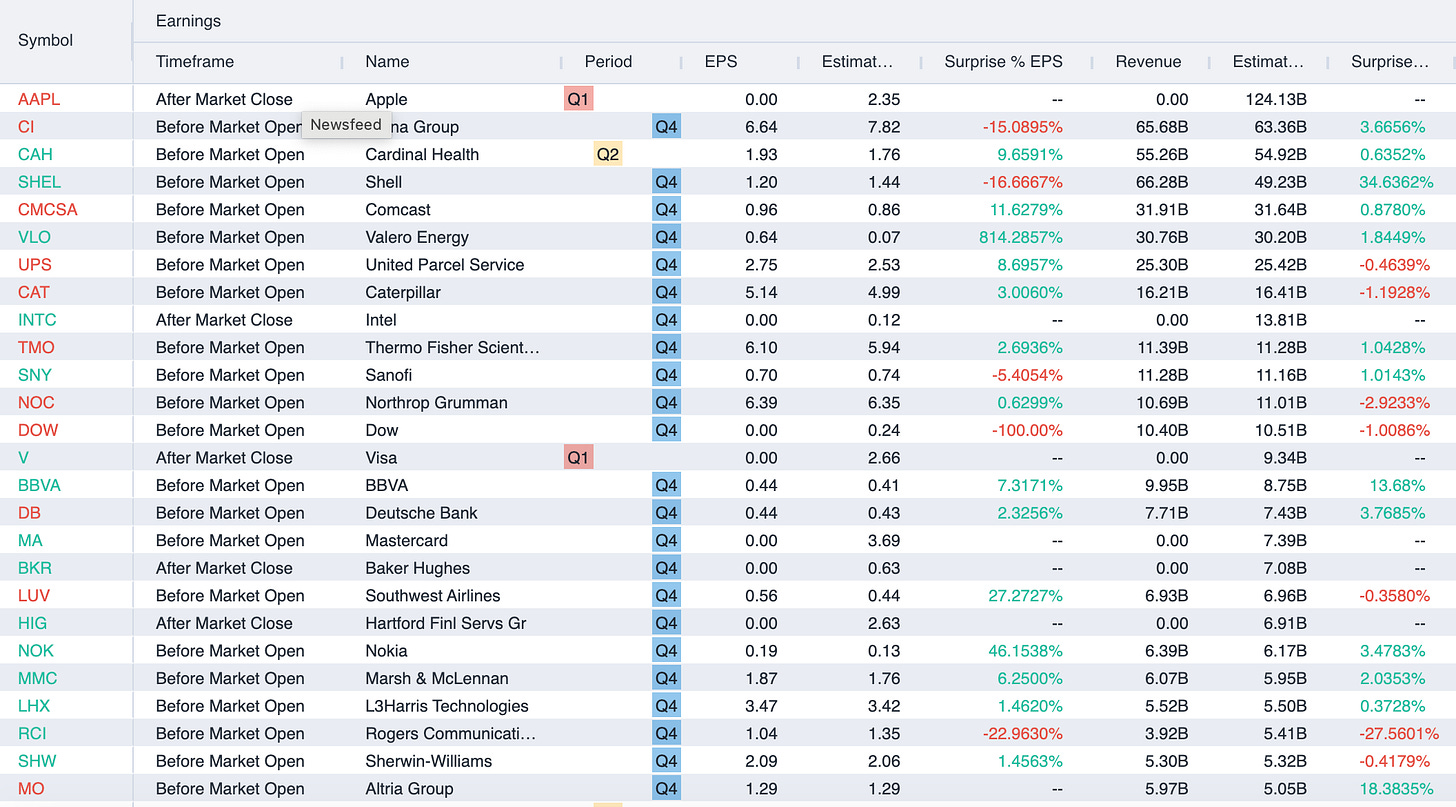

Another big day of earnings - Apple, and Visa after the close. MasterCard, Caterpillar and UPS before the open.

Calendars

(news taken from Reuters, FT, Bloomberg; Calendar from Trading Economics)