Rise and shine everyone.

The markets are viewing the latest tariff measures between the US and China as less severe than they could have been, both in scale and scope. Tariff uncertainty lingers, but China’s measured retaliation keeps investors on edge. A temporary reprieve from US tariffs on Mexico and Canada has provided some optimism, though China’s probe into Apple’s app store fees suggests tensions remain. Trump has signaled that he will discuss trade issues with Xi Jinping “at the appropriate time,” leaving room for potential de-escalation.

However, the US Postal Service announced a temporary suspension of international package acceptance from China and Hong Kong starting February 4th, a move seen as exposing a large-scale manufacturing and logistics scheme benefiting Chinese companies at the expense of US industries.

In China, the Shanghai Composite initially opened higher after the extended Lunar New Year break but quickly turned negative, mirroring the Hang Seng. Several partners of China’s DeepSeek surged as trading resumed. The January Caixin Services PMI remained in expansion for the second year but came in lower than expected, marking its weakest reading since September 2024.

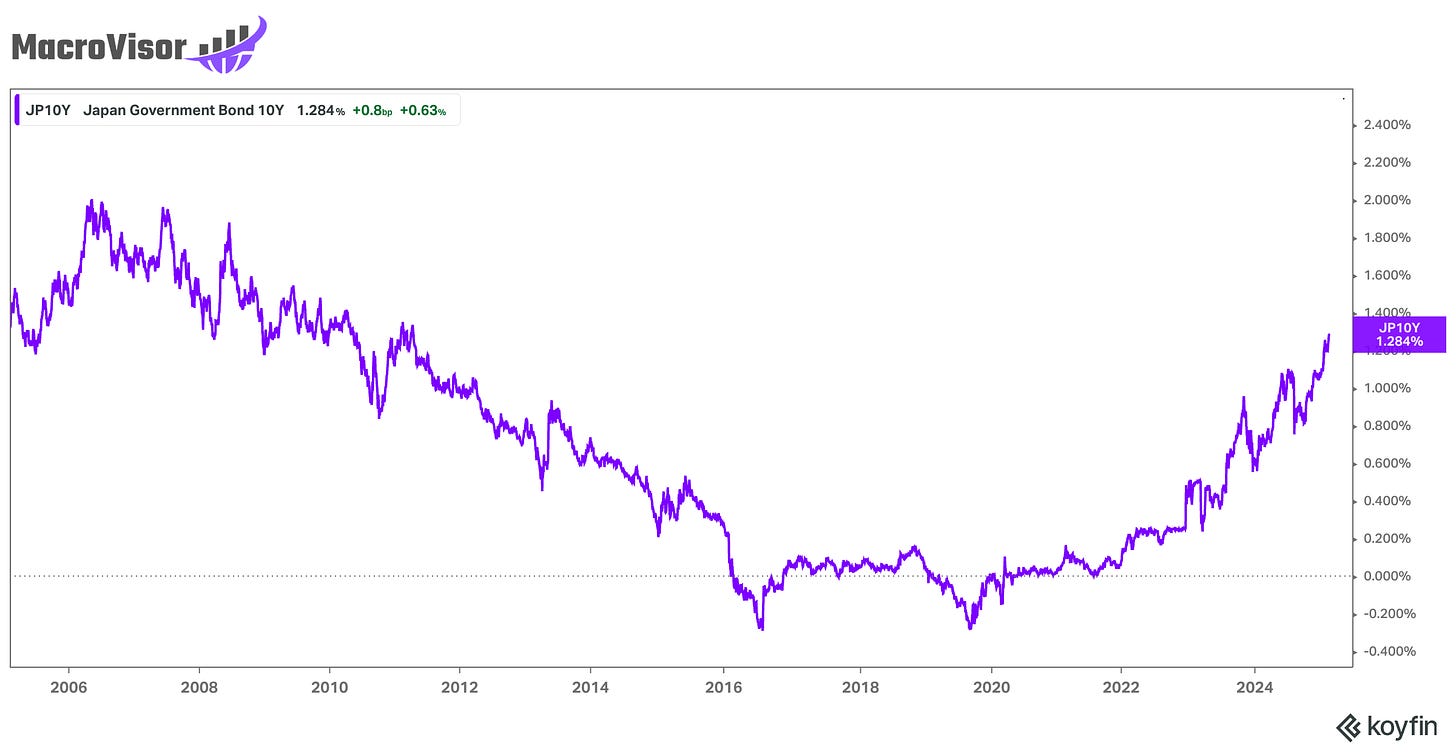

Japan’s Nikkei reversed early gains as expectations for further BOJ rate hikes grew, fueled by former BOJ official Hayakawa’s prediction of two more increases in 2025. The Yen strengthened across the board, reaching a six-week high against the USD, dampening sentiment. However, Toyota shares jumped 5% on strong earnings and plans for a new EV battery factory in Shanghai, helping the Nikkei recover. Japan’s December cash earnings saw a larger-than-expected increase due to a 6.8% rise in winter bonuses, while the final services PMI improved from preliminary readings. This lead to further convictions about more rate hikes and the 10-year JGB yield continued its climb, reaching 1.297%, the highest level since April 2011.

South Korea’s Kospi outperformed the region, rising 1.3%. Inflation climbed above the 2.0% target for the first time in seven months, though the BOK maintained that inflation should stabilize near target going forward.

In the US, weaker tech earnings saw GOOGL drop 7.3% and AMD fall 8.8% after hours.

President Trump reiterated his focus on federal cost-cutting and is reportedly considering revoking loans for the $400B Office of Clean Energy Demonstrations. His statement that the US should take over and develop Gaza was swiftly opposed by Saudi Arabia and Australia.

Gold hit a record high of $2,848/oz, while the US Dollar is seeing weakness this morning.

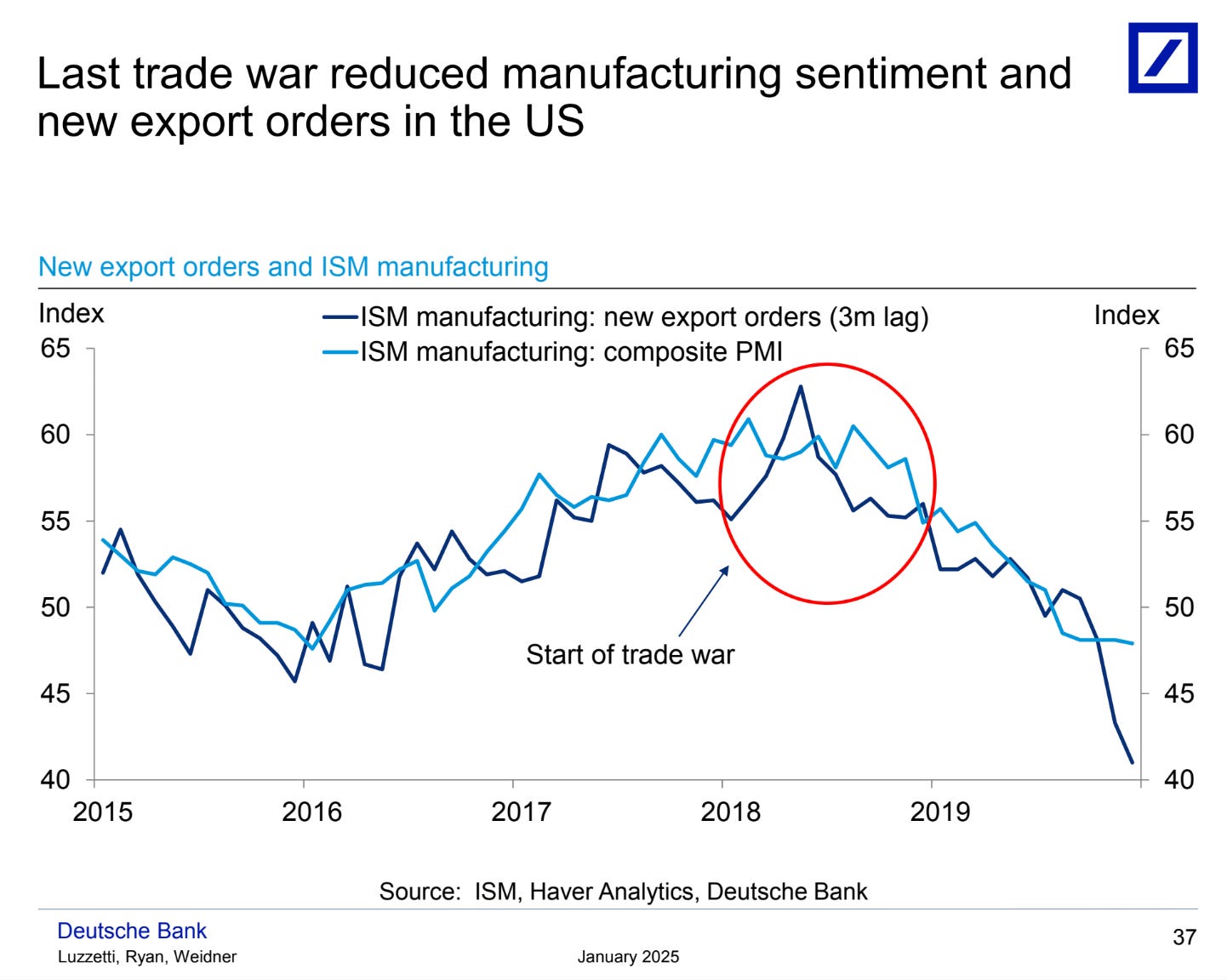

Chart of the Day - Trade Wars are not good

While the last reading of the ISM Manufacturing PMI for the US finally crossed over into expansionary territory after 26 months, this may not continue to remain the case. The report earlier this week showed that a significant part of this was driven by New Orders. During the last trade war with China, however, new orders plummeted. So this will be an important metric to keep an eye on, going forward.

What We’re Watching

US ISM Services PMI numbers to be released at 10 am ET

Potential developments in the US-China Tariff situation

Calendars

(news taken from Reuters, FT, Bloomberg; Calendar from Trading Economics)