Rise and shine everyone.

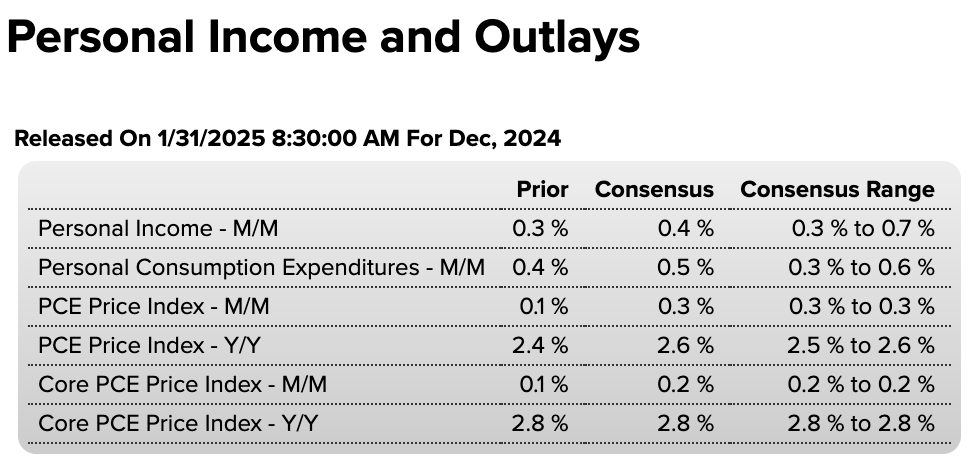

Happy Friday! Today’s focus will be on the PCE Inflation numbers coming out of the US at 8:30 am ET. The consensus is for slightly elevated numbers for December compared to November.

This should come as no surprise given the US GDP numbers we saw yesterday. While overall GDP Growth slowed in the fourth quarter to 2.3% from 3.1% QoQ, personal consumption growth remained resilient. On a quarterly basis, personal consumption grew 4.2% vs. the estimate of 3.2% and the prior Q3’s actual 3.7%, which was already a robust number. The drag on GDP came mainly from non-residential fixed investment, and to some extent exports. I won’t be surprised if we’re rather seeing imports surge to stockpile ahead of impending tariff announcements.

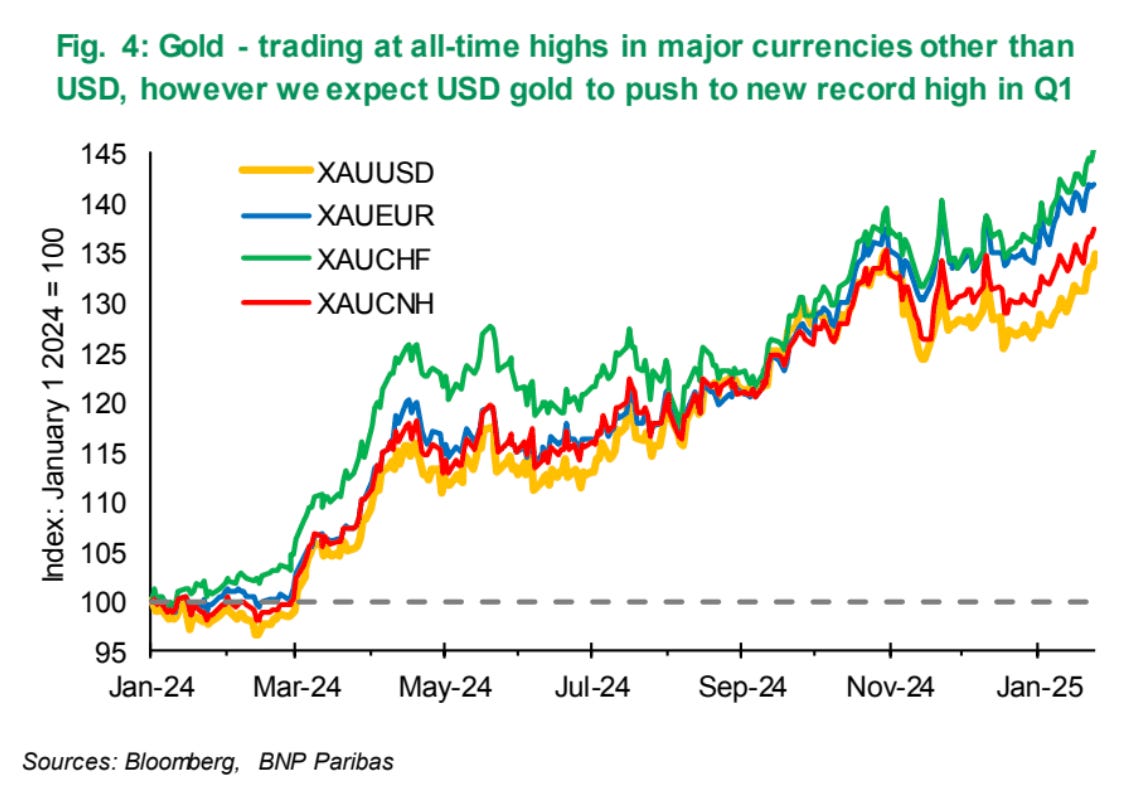

Speaking of tariffs, President Trump is set to roll out his first wave of tariffs at 25% tomorrow, with Canada and Mexico, two of the biggest buyers of U.S. goods. 25% is a lot and there’s some discussion that some of this may be renegotiated down the road. Commodities markets are on edge, and many traders are buying up gold apparently as a safe haven.

Gold prices have reached an all-time high in almost every currency.

In other news, the ECB went ahead and cut 25bps, as expected. We got German retail numbers this morning that show a significant drop from -0.1% in November to -1.6% in December. The German Retail economy is not doing well.

Meanwhile, geopolitical tensions continue to escalate. Senator Marco Rubio backed President Trump’s controversial proposal to buy Greenland, emphasizing that it’s not just a far-fetched idea but a strategic concern. The argument: If the US doesn’t act, China might potentially use Greenland to expand its military and economic influence, something Washington is keen to prevent.

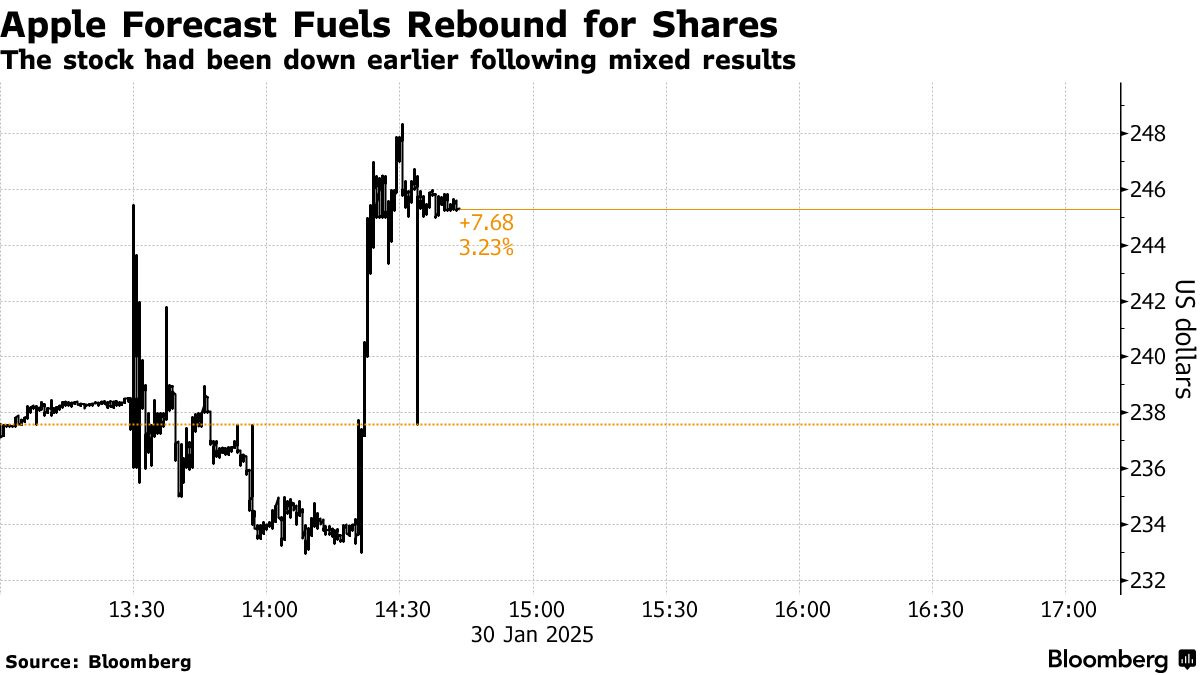

Finally, Apple reported a miss in iPhone numbers yesterday but provided a reassuring revenue forecast, expecting low- to mid-single-digit growth, which helped ease investor concerns despite mixed holiday results. The company faced a sharp 11% revenue decline in China to $18.5 billion, missing estimates, while iPhone sales dropped slightly to $69.1 billion. CEO Tim Cook attributed China’s weakness partly to inventory issues, while also acknowledging Apple’s slower AI rollout compared to competitors. Despite challenges in AI, wearables, and international regulatory scrutiny, strong services revenue (up 14% to $26.3 billion) and better-than-expected Mac and iPad sales boosted overall revenue by 4% to a record $124.3 billion. As Apple works on a major iPhone refresh and expansion of AI capabilities, shares rebounded more than 3% in premarket trading.

Chart of the Day

Precious metals are still well bid, while copper is marginally pulling back. US Equity Futures are looking better this morning but, the US 10Y Yields are higher. A disappointing inflation reading, combined with the tariff discussion, could push the 10Y yield to 4.75% and put pressure on equities.

What we’re watching

PCE Inflation Numbers at 8:30 am ET

Updates on the Tariff situation with Mexico and Canada

Earnings Call updates from ExxonMobil, Chevron, Charter Communications

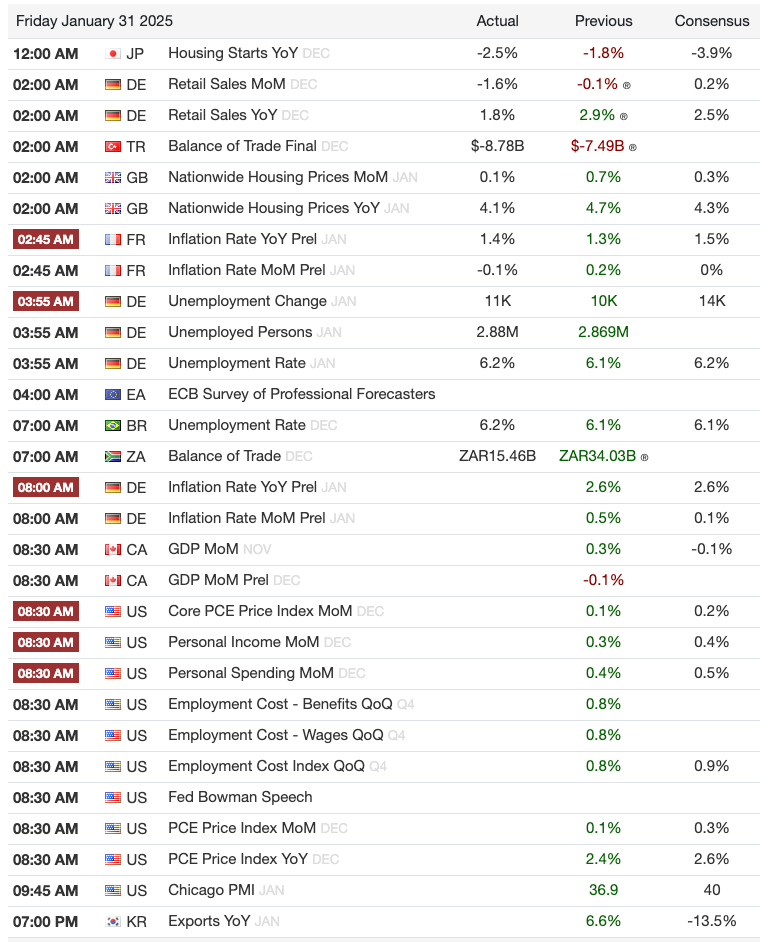

Calendars

(news taken from Reuters, FT, Bloomberg; Calendar from Trading Economics)