Earnings season starts in full flow this week and so far the banks have done a tremendous job setting the tone with better than expected numbers.

We have a host of important earnings this week and we’re covering them, as always, from a macro perspective. We’re not making predictions here but, more importantly what we should be looking out for and what they tell us about the economy and the markets as a whole.

We’ve decided to move to a written format so that you can pick and choose the earnings / sector that most interests you.

Market Update

S&P 500

Earnings Scorecard - S&P 500

So far, we’ve had 34 companies in the S&P 500 report with an actual EPS growth of 16.12%. This brings the blended earnings growth to a +0.41%. The blending earnings is the actual earnings + estimated earnings for all the companies in the index. As we move through earnings season, blended earnings = growth reported.

Nasdaq-100

For the Nasdaq-100, we’ve had 8 companies report with an actual growth rate of -19.51%. This metric is a bit skewed here because of one major earnings which is Micron Technologies who reported a -173% decline in EPS. Other than that, we have Walgreens who reported a decline of -16% under health technology.

This Week’s Earnings

Earnings covered in this update

(Need new image)

Automotive

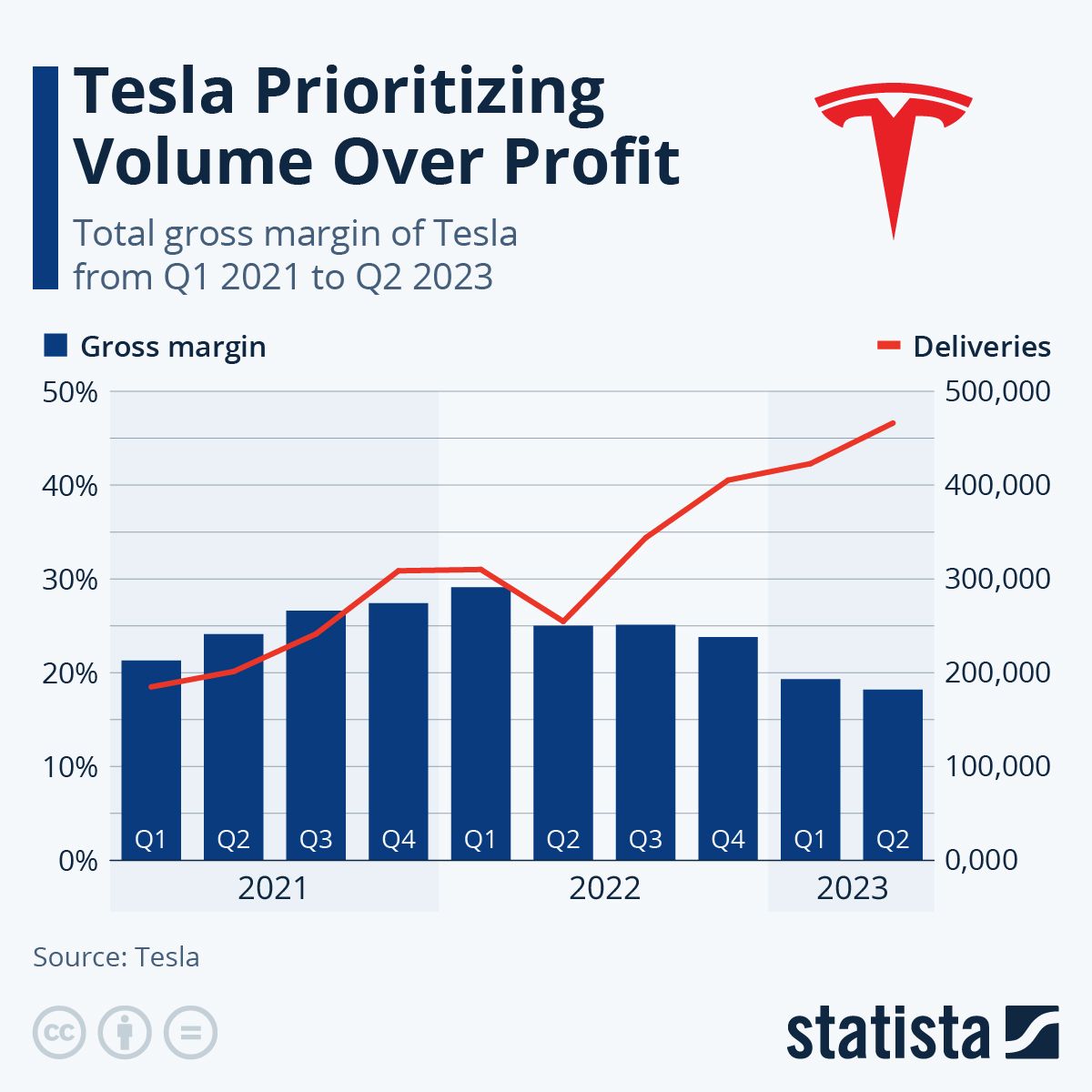

Tesla (TSLA) - Reporting 18 Oct 2023 (AMC)

EPS est: $0.73; Revenue est: $25.255B

This could be a tough quarter for the automaker, given slowing EV sales and missed deliveries at just 435K during Q3.

Inventories are building and production has slowed, reaffirming the idea that management sees slowing sales as a trend that could continue to challenge the business’ once promising growth trajectory.

The headwinds we’ll be watching closely are as follows:

Competition is increasing and Tesla is beginning to lose global market share, particularly in China.

Auto sales slowing is likely to erode revenue as other business segments are very unlikely to make up for the difference in revenue.

With further price cuts, including to FSD, margins are likely to experience continuing pressure both in Q3 and within guidance for Q4. Cutting prices initially helped to improve volume, but that impact may be diminishing.Tesla advertising?

Tesla advertising? Influential shareholders want to see the company begin to embrace marketing, but company has consistently hesitated. Musk has used X to promote Tesla aggressively, but outside of that there’s no traditional advertising presence of yet. Any signs of a sales and marketing engine being built could be seen as encouraging.

Ultimately, Tesla remains a car company, with auto sales accounting for the vast majority of its revenue. The benefits of regulatory credits have been diminishing over the last year, reducing one tailwind for growth.

How Tesla performs in the increasingly competitive EV space will be crucial for investors to determine how management is executing within a more challenging macro environment.

Healthcare

The only thing anyone wants to talk about in healthcare these days is the GLP-1 drugs (the weigh-loss drugs). And to be fair, I would like to hear what all these companies have to say as well. While all of this will take time to unfold, I’m sure this will be a major point of discussion and healthcare companies would be prudent to plan for it. Let’s look at the effects on healthcare:

Medical Devices and Drugs - J&J, Abbott, Intuitive Surgical - all thrive on medical conditions that are side effect of being overweight. A major reason for heart surgery, orthopedic surgery, and kidney issues are because of obesity and alcoholism.

Elevance - Insurance - Fewer visits to the doctor will mean lower insurance revenue. Now, here the question will be how much of these weight loss drugs is covered by insurance. There’s still no clear indication about that.

US Dollar and Overseas Demand - The stronger dollar will have a negative impact on J&J, Abbott and ISRG. There was also discussion about the slowdown in demand from China for medical equipment so that’s something we’d keep an eye on.

These companies have given up most of their gains from the gap up on previous earnings. I am wary about how much of that pent-up demand still gives their earnings a tailwind during this quarter.

Mining

Alcoa (AA) - Reporting 18 Oct 2023 (AMC)

EPS est: -$1.06; Revenue est: $2,585M

Alcoa hasn’t had a great run. Even with the spike in Aluminum prices over the last few months, Alcoa hasn’t really seen a spike in their prices because of higher energy costs. Aluminum production is extremely energy intensive.

We’ve seen the global manufacturing PMIs - they’re not looking great. Construction activity has slowed considerably worldwide. China has their own sources of aluminum and they’re likely to be more of buyer from Rusal (Russia). The shutdown of manufacturing facilities did present an opportunity for Alcoa but, the slowdown in activity overshadowed this.

If China continues to ration their refining and smelting capabilities, Alcoa may get a bid. I think the most important thing would be to keep an eye on the tonnage of production for this one and what they see in terms of demand.

Freeport-McMoRan (FCX) - Reporting 19 Oct 2023 (BMO)

EPS est: $0.34; Revenue est: $5,403M

Unlike Alcoa, FCX has actually managed to fare better in the face of declining copper prices.

FCX has a budget of $4 and A 10c increases or decreases their P&L by $315m. Last quarter their volumes came in slightly lower for Copper by -3% but their realized cash price was better than expected at $3.84 given the market circumstance. A few things to look out for:

During the Morgan Stanley conference, FCX discussed how China’s demand for copper is still growing because of the surge in EVs. While this is a great view on copper and I think we will see bullishness in pricing, it’s likely a slower transition that will take longer than 2-3 quarters.

In the immediate term, concerns about the economy will be front and center and China’s property market decline. A discussion on US housing supply may also come into the conversation. EPS Consensus

On the supply side, there were concerns about mining permits in Indonesia and worker shortages in the US.

Finally, we think there will be repercussions from the auto manufacturer strikes as that is major source of demands.

Transportation

EPS Consensus

The Transportation Industry has been displaying relative strength. This is more so because of trucking rather than rails. While intermodal / container traffic has also picked up, trucking volumes have picked up far more for the same reasons - inventory replenishment.

Trucking volumes have increased substantially over the last quarter. In Q1 and Q2, we had a situation where companies had over-stocked and needed to get rid of their inventory. So, they weren’t ordering new volumes as much. This has changed during the summer. AS you can see from the image below, April to August saw an increase.

Last quarter’s earnings brought us a lot of discussion a freight recession but, we’ve firmly moved past that since then. We still want to look out for whether spot rates are lower than contract rates. That would bring freight rates down further. But, as of know, freight margins remain high compared to historical levels.

There is still a lot of trucking capacity in the market (despite the bankruptcy of Yellow). During the pandemic a lot of small truckers came into the market and

What we will be looking for:

The price of diesel - larger trucking companies actually make more money when the price of diesel is going up because they are able to buy wholesale and pass on the higher cost to customers. Smaller trucking companies don’t have this advantage and usually buy at the pump at retail rates.

Volumes going into the holiday season. This will give us great insight into how the holiday season will look like for retail.

UAW strikes - According to FreightWaves, most recent data in September, early October shows a drop off in volumes of -12% and they speculate this is likely because of lack of shipment of auto parts. Auto manufacturers use more just-in-time inventory systems and therefore, use trucks and air transport as opposed to the slower rail transport.

Whether the increase in the cost of debt, i.e., higher rates are hurting smaller companies. Trucking is a debt-intensive business, and the Oct 17-20 2023smaller companies that have slimmer margins may find it difficult not only to borrow new debt but, also to pay back existing debt.

Credit Cards and Consumer Lending

We saw what JP Morgan reported in terms of Credit Cards. They discussed a lower level of provisions but a higher level of net charge-offs. One important I just busted out some of the last of my White Burgendy point that they highlighted was that consumer spending is slowing to pre-pandemic levels. So what we will look out for with the card companies:

Delinquencies and defaults

Consumer lending growth

Here’s the chart we present on the credit card data. Clearly none of the companies are doing as great anymore.

But if you stack them up in terms of defaults, clearly the banks and American Express is doing much better than Capital One, Synchrony and Discover.

Semiconductors

The semiconductor space continues to face pressure from a drop in global demand, outside of niche areas such as GPUs for AI acceleration. Though we are seeing some signs that in Q3 demand is beginning to improve across the entire space.

Global semiconductor sales via FactSet

Q3 earnings will be very interesting to digest as a result. We do not expect a significant broader industry rebound this quarter, but potentially signs of a trough in Q2, with Q3 sales increasing quarter-over-quarter, but still lower than where they were in Q3 2022.

For example, computer and mobile phone sales remain rather low year-over-year from various surveys. Overall consumer electronics sales and spending plans have also fallen, with electronics spending falling markedly in September based on credit card spending data.

Taiwan Semiconductor (TSM) - Reporting Oct 19 2023 (BMO)

EPS est: $0.34; Revenue est: $5.403B

Taiwan Semiconductor is facing increasing competition, even the company's founder is concerned about the future. The lack of globalization is one driving factor (or, put another way, re-shoring and friend shoring). Revenue has been falling year-over-year at the company over the last three months, but does show improvement over Q2.

Source: Taiwan Semiconductor Investor Relations

ASML - Reporting Oct 18 2023 (BMO)

EPS est: 4.92; Revenue est: $7.188B

Canon plans to take on ASML in more sophisticated manufacturing of chips, but those impacts are further in the future. Overall the company's larger risk is the diminished sales to China due to trade restrictions and a slowing of reinvestment by major semiconductor producers, however, and price hikes could pose a further challenge therecers due to their own inventory gluts reducing capex.

These latter impacts may be at least partially offset by the need to stay competitive by innovating more advanced chips within the AI and data center spaces.

What we are watching in the industry:

Signs of a recovery in revenue from multiple players in the spacehowever, and price hikes could pose a further challenge there, and whether Q2 or Q3 is likely to be the trough, particularly within Oct 17-20 2023consumer electronics.

Guidance, particularly looking ahead to 2024 and whether expectations remain for a stronger resumption in spending

Potential for further margin compression from having to move inventory at lower prices or stabilization, indicating management is more confident about demand.

Signs that excess inventory has been drawn down, to add to the color from the above data.

Telecom

AT&T (T) - Reporting Oct 19 2023 (BMO)

EPS est: $0.62; Revenue est: $25.25B

DirecTV continues to languish. The 70% stake may be sold off.

5G offerings are catching up with Verizon and T-mobile as build-out is beginning to pay off in terms of end user experience, speed, coverage

Lead cable risks seem to have been overstated, recent tests show less contamination than thought

Will be important to monitor cost cutting efforts and whether subscriber additions continue, helping to boost bottom and top line growth

What we’re watching:

Whether 5G improvements are paying off with less churn and improved growth for new and returning subscribers

If 5G spend has peaked and we may begin to see further cost improvements leading to better margins

Further guidance from management that lead cable issue was overblown and potential future liabilities are much lower than projected by WSJ

Broadband growth trends and whether AT&T’s fiber offerings are seeing improved market share in areas where they compete against cable companies with more limited bandwidth speeds and reliability

Streaming

Netflix (NFLX) - Reporting Oct 18 2023 (AMC)

EPS est: $3.49; Revenue est: $8.538B

More price hikes coming, likely to boost revenue and earnings. The platform is relatively sticky in key geographies, such as the US and Europe where most subscribers reside. There continue to exist opportunities to grow in less saturated, particularly within Japan, South Korea, and other parts of Asia.

Netflix geographic revenue composition via FactSet

Subscriber growth is picking up again, which may be giving the confidence to raise prices as they expand their offerings.

Netflix subscriber growth via Statista

Management is putting more effort into video game production to diversify revenue streams and attempt to capture the fastest growing space in multimedia, but this has proven to be a very difficult space for others to break into. It will be very important to monitor how well management executes in this space as it could be either a cash furnace or a significant growth engine.

Netflix original content spend and selection are both growing. This is encouraging as the value of the platform is the experience it delivers to the customer, and there had been a period of lower original content production which caused overall retention trends to drop.

The company's plans to launch retail stores in 2025 are strange, and a potentially unnecessary spend. Calls into question management's vision, but we will keep an open mind for now.

What we are watching:

Signs of continued subscriber growth to bolster the idea that price hikes are the right decision.

Further improvement of margins as the company continues to reduce costs.

More guidance on how management is executing within the video game production space.

The cessation of the writers strike leading to content production resuming full speed ahead — and any discussioOct 17-20 2023n by management of their plans for 2024.

How capturing new markets is progressing with content created specifically for those geographies, particularly within South Korea, Japan, and India.

Defense

Lockheed Martin (LMT) - Reporting Oct 17 2023 (BMO)

EPS est: $6.67; Revenue est: $16.731B

Lockheed may continue to see a boost from increasing geopolitical instability in the Middle East and the sustained conflict between Russia and Ukraine. The unfortunate reality of a more chaotic and conflicted world is that defense contractors tend to benefit with greater demand for their products and services.

A large amount of replenishment of weapons and ammo needed due to weapons and ammunition being sent to Ukraine is likely to be a theme we hear more about.

The US defense budget continues to increase as a result of both of these factors, with spending increasing to $884B in FY2024, another tailwind for the government contracting operations of Lockheed, its mainstay.

Lockheed’s Joint Strike Fighter program is objectively a disaster, but ironically a a highly profitable disaster with recurring high maintenance costs that cannot be insourced by DoD due to the technological complexity of the fighter.

What we are watching:

Any concerns regarding potential government shutdown impact on Q4 (could make revenues more lumpy, defer some spending).

Further detail on what global defense spending trends look like in a more conflicted world, and how that may impact sales trends.

Upside surprises in revenue and earnings due to higher than expected demand for weapons and ammunition in Q3.

If you have any questions or feedback, let us know in the comments below. Have a great week!