We get key inflation data this week with both PPI and CPI coming out, and in opposite order as they usually do, with PPI first tomorrow and then CPI on Thursday — both alongside longer duration Treasury auctions which could make interpreting the data even more interesting.

To start off, here's a recap of the Consumer Price Index (CPI), Producer Price Index (PPI), and the notable increase in diesel prices fro August’s data print in September.

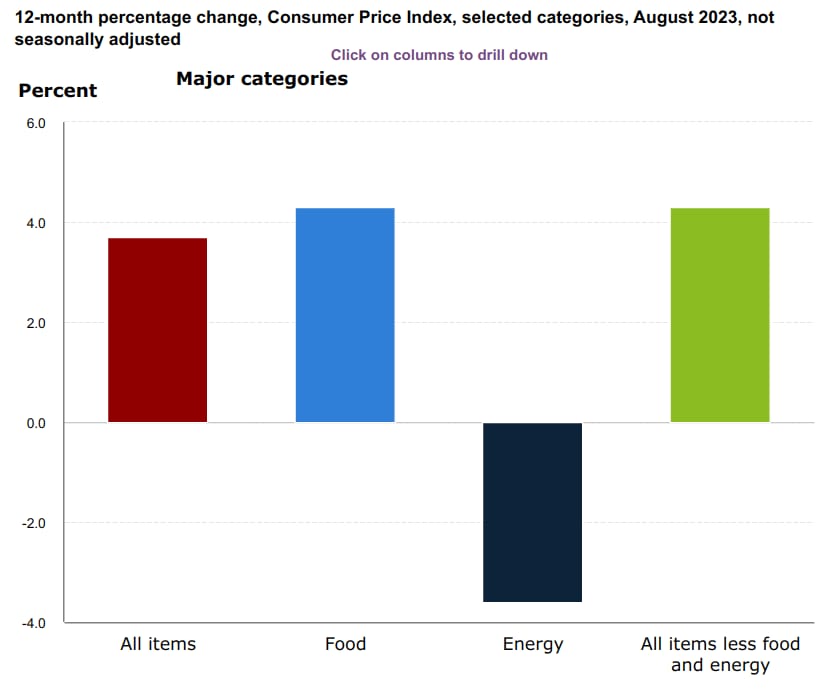

Consumer Price Index (CPI)

The Urban CPI increased by 13.9% on an annual basis (September 2023 compared to September 2022) and by 3.6% on a monthly basis (September 2023 to August 2023).

Analysts are watching closely to see how core CPI (which excludes food and energy prices) performs.

Core CPI, which excludes volatile food and energy prices, was expected to increase by 4.2% annually and 0.4% on a monthly basis.

The overall measure of the CPI increased by 3.7% year-over-year from August 2022 to August 2023.

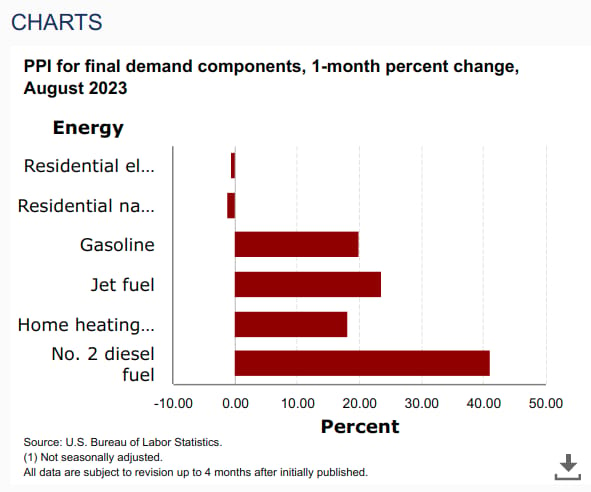

Producer Price Index (PPI)

The PPI data focuses on what producers are paying, and can help to provide clues about the direction of CPI over the following 2-3 months, particularly if price increases are broad and large enough that they are more likely to be passed on.

Last month there were a few interesting areas to highlight:

In the US, producer prices increased by 0.7% in August 2023, exceeding market expectations of a 0.4% rise.

This increase was driven by a 2% advance in goods prices, and a significant 10.5% surge in energy costs was noted

Diesel Prices

With the growing shortage in diesel a key concern, last month’s PPI data showed that prices rose significantly, and there are signs that this may be part of a larger trend:

A 41% month-over-month rise in diesel prices for September 2023 occurred in PPI data because of a convergence of factors, including limited refining capacity and availability of sour crude and diesel imports from producers like Saudi Arabia and Russia.

The national average retail diesel fuel prices continued to rise during the month, hitting $4.54 per gallon as early as September 11th.

The average price per gallon was $4.56 for the month, suggesting that the price rise lasted long enough to put upward pressure on input costs for many industries.

A global diesel shortage, low distillate inventories, and rebounding manufacturing activity are among the factors contributing to upward pressure on diesel prices.

The rising prices, particularly in energy costs and the upward trend in diesel prices, alongside the notable increases in both CPI and PPI, suggest growing inflationary pressures.

The surge in diesel prices, in particular, can have ripple effects across various sectors, notably transportation and manufacturing, which in turn, may further fuel inflation.